7 Medicare Enrollment Questions Every Beginner Needs to Ask

With the ever-changing rules and regulations, enrolling in Medicare can be confusing and difficult without the right guidance.

But understanding the basics of Medicare eligibility and enrollment can help you make sure you’re getting the coverage you need.

To make the process easier, we've put together a list of 7 common questions (and answers!) about Medicare enrollment.

Your Guide to Medicare Parts A & B

Understanding your Medicare options is important, because making a decision without the facts can cost you money. See what Medicare, Medigap, and you – pay for.

Get It Now

Medicare Basics

Medicare is a federal health insurance program designed to help people over the age of 65, as well as those with certain disabilities and end-stage renal disease, pay for medical expenses. It is administered by the Centers for Medicare & Medicaid Services (CMS).

When you turn 65, you’ll be able to choose from a variety of plans that offer coverage for hospital visits (Part A), doctor visits and other medical services (Part B), prescription drugs (Part D), and sometimes additional coverage options like skilled nursing facility care or hospice care.

Depending on the plan you choose, your premiums, co-pays, deductibles, and out-of-pocket costs may vary.

It’s important to carefully consider all your plan options before enrolling in Medicare to ensure that you get the best coverage at the lowest cost possible. Enlisting the help of an experienced insurance broker can really help you sift through the plan options and choose the one that suits you best.

You can get a lot more information about Medicare options and enrollment periods in the Official Medicare & You Handbook.

1. Do I have to sign up for Medicare if I don’t want it?

If you are eligible for Medicare and you don't want it, you aren't required to enroll in the program. However, if you decide not to enroll in Medicare when you first become eligible and you do not have other creditable coverage, you’ll start accruing penalties that kick in when you do sign up for Medicare in the future.

Additionally, delaying enrollment can mean missing out on important benefits like prescription drug coverage and medical insurance that may only be available through Medicare.

So, it's important to consider your options carefully before deciding whether or not to enroll in Medicare.

2. What happens if I don’t want Medicare?

If you don't want Medicare, you don't have to enroll in it, especially if you're getting health insurance from somewhere else, such as your employer or your spouse's employer.

However, as we mentioned above, you will start accruing penalties that will be charged later when you do sign up for Medicare. Generally, you will accrue a penalty for each month you go without Medicare.

Also, if you don't enroll in Medicare when you are eligible and don't have other health insurance coverage, you may be responsible for paying the full cost of your medical expenses out of pocket.

3. When do I sign up for Medicare if I’m still working?

If you or your spouse are still working and have employer-provided health insurance, you may not need to sign up for Medicare when you turn 65. However, you should weigh the pros and cons of your employer group plan vs Medicare. Many times, switching to a Medicare plan instead of your employer plan can save you a ton of money.

That said, there are some instances where an employer plan has better coverage. If that is the case for you, you can delay enrolling in Medicare until you leave your job or retire.

At that time, you will qualify for a special enrollment period. This special enrollment period lasts for eight months from the month that you or your spouse stops working or from the month that your employer-provided health coverage ends, whichever happens first.

4. Do I have to sign up for Medicare if I have private insurance?

If you have private health insurance, you may not need to sign up for Medicare. But it is important to consider all your options carefully and make sure that your private plan covers everything you need, or how your private insurance and Medicare coverage may work together.

For example, if your private plan does not cover prescription drugs or has a high deductible, then it might be worth considering signing up for Medicare in addition to your private coverage.

Your private insurance may still be your primary coverage and Medicare may be secondary, depending on the terms of your private insurance plan. This means that your private insurance would pay for covered services first, and Medicare would pay for any remaining costs.

Also, remember that some private plans may no longer offer coverage once you turn 65, so it is important to check with the company if this applies to you.

5. What happens if I don’t sign up for Medicare Part A at 65?

If you're already receiving Social Security benefits or benefits from the Railroad Retirement Board, you will automatically be signed up for Medicare Part A when you turn 65.

And if you're under 65 and have a disability, you'll automatically get Part A after you get disability benefits from Social Security or certain disability benefits from the RRB for 24 months.

In most cases, as long as you or your spouse paid Medicare taxes while working for 10 years, you'll pay a $0 premium for Part A coverage. So even if you don’t use it or have another insurance, there's no harm in having it.

6. What happens if I don’t sign up for Medicare Part B at 65?

If you're already receiving Social Security benefits or benefits from the Railroad Retirement Board (RRB), you will also automatically be signed up for Medicare Part B when you turn 65.

If you don't want Part B, you must let Medicare know before the coverage start date on your Medicare card. You'll get that card in the mail 3 months before your 65th birthday or the 25th month of disability benefits.

If you're NOT getting Social Security or RRB benefits, you'll have to sign up for Medicare Parts A and B. You can do this on the Social Security website. If you worked for the railroad, contact the RRB.

If you miss your initial enrollment period for Medicare Part B, and you don’t have another creditable coverage, you’ll end up paying a late enrollment penalty for the months you were not covered when you do sign up for Medicare Part B later down the road.

The late fee will be an extra 10% for each year you were eligible but went without coverage, and it will be added to your monthly Part B premium. It's not a one-time fee, either – it's for life.

7. Do I automatically get Medicare when I turn 65?

Most people get Medicare Parts A and B automatically when they turn 65, because they are getting Social Security or RRB benefits.

As a reminder, Part A covers inpatient hospital care, skilled nursing facility, hospice, lab tests, surgery, and home health care. Medicare Part B covers doctors and other health care providers' services and outpatient care.

If you're still working and not yet getting benefits from Social Security or the RRB, you won't get Medicare automatically.

Conclusion

There's a lot to consider when it comes to enrolling in Medicare. Take the time to educate yourself on the enrollment process so that you can make informed choices before it's too late to enroll.

Luckily, our team of licensed sales agents can lend a hand!

We'll help you figure out the timing, enrollment windows, and any fees you might rack up if you don't enroll on time. Plus, we can also assist you with the sign-up process, making it even easier for you. It's best to reach out about 6 months before your 65th birthday, so schedule an appointment or give us a call as soon as you're ready.

And if you're not quite ready to sign up yet, but want to learn more about Medicare, we've also got you covered. Our team member Michael Sams hosts free educational seminars that can help answer your questions. Grab your free tickets today!

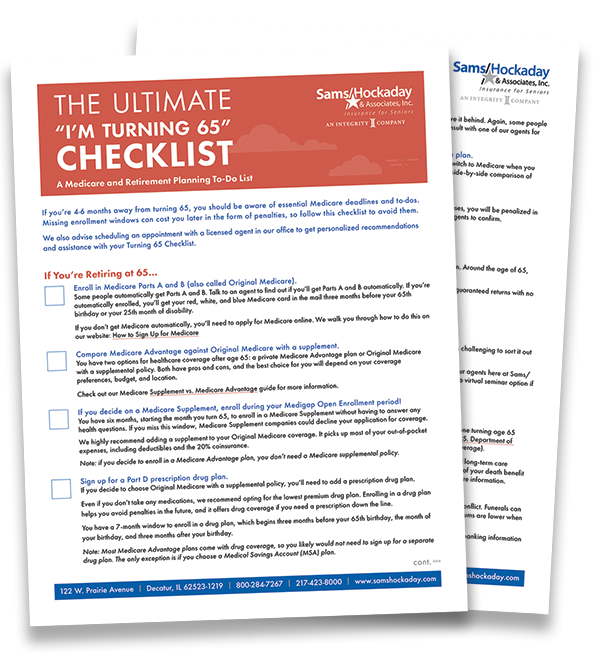

Get Your “I'm Turning 65” Checklist

Are you turning 65 soon? Avoid missing critical Medicare enrollment deadlines with this Turning 65 Checklist.

Get My Checklist

Here's what our clients say…

Meet Our Agents