If You Don’t Understand Medicare At All, Start Here

We’ve all been new to Medicare at some point, and even folks who have had Medicare coverage for years don’t fully understand it.

It’s a complex health insurance system with all sorts of acronyms, loopholes, and pending legislation.

But alas, you have to start somewhere.

If you don’t understand Medicare at all, start here.

Calculate Your Medicare Costs Today

Create a Medicare action plan by estimating your total monthly premiums for healthcare and related expenses in retirement.

Get My Worksheet

What the heck is Medicare?

Medicare is a government-led health insurance program for people ages 65 and older. There are a couple exceptions, but for most people, you’re eligible for Medicare when you turn 65.

Medicare is governed by an organization called CMS, which stands for the Centers for Medicaid and Medicare Services. (If you get anything in the mail from CMS, don’t toss it!)

While there are lots of nuances (naturally), here's the simplest explanation of Medicare coverage: Medicare pays for around 80% of your doctor and hospital bills in retirement.

Is Medicaid different from Medicare?

That brings us to our next question – what's Medicaid?

Medicaid provides health coverage for Americans of any age who have a low income.

If you’re a household of two in Illinois, you need to make less than $24,040 per year to qualify for Medicaid (as of 2021). If that might be you, you could be dual-eligible – eligible for both Medicaid and Medicare. In that case, Medicare and Medicaid would work together to cover your eligible medical costs. So, instead of around 80% coverage, you'd be 100% covered for all Medicare-approved expenses. (Medicare doesn't cover everything.)

Isn't Medicare free?

Medicare is not free. A lot of people think it is because they've paid into the Medicare program their whole lives. But unfortunately, it's not.

It’s probably a lot cheaper than the health insurance plans you’re used to, but it’s still not free.

Even if you don’t purchase any supplemental coverage, you have costs with Medicare.

What are the parts of Medicare?

Medicare has several parts, but the two main parts are Part A (hospital coverage) and Part B (medical coverage).

You’ll often see Parts A and B referred to as “Original Medicare” since they were the first parts of Medicare when it started.

How much do the parts of Medicare cost?

For most people, Part A is $0 premium, so that’s a big plus. But Part B’s premium is $148.50 per month (in 2021).

Another thing many don’t realize is the higher your income, the more you pay for Medicare.

For example, most people pay the standard $148.50 per month for Part B’s medical coverage. But if you have a high income (above $176,00 for couples filing taxes jointly), you could pay anywhere from $207.90-$504.90 per month (in 2021).

In addition to Medicare premiums, you also have copayments, coinsurance, and deductibles. Earlier in this article, we mentioned that Medicare covers around 80% of your healthcare costs. To help with the other 20%, you really need a Medicare Supplement. (There's an entirely different path you can take, but we'll get to that in the next section.)

Medicare Part D, or prescription drug coverage, also comes with its own premium, deductible, and copays at the pharmacy.

If you don’t take any medications or only take generic prescriptions, you can get a really inexpensive drug plan ($10 or less per month) to have as a backup – plus, it helps you avoid future penalties. That’s right – you’re penalized if you don’t sign up for a drug plan, but that’s a story for another day.

Read up on that topic here: Penalties For Not Signing Up For Medicare Part D: What Is the Part D Penalty?

You probably noticed we’ve mentioned Parts A, B, and D – what about Part C?

What Is Part C… or Is It Medicare Advantage?

Part C, more commonly referred to as Medicare Advantage, is an alternative option to Original Medicare.

In simple terms, when you’re eligible for Medicare (typically at age 65), you have two paths to consider:

- Stick with Original Medicare, and consider adding a Medicare Supplement and Part D drug plan

- Forfeit Original Medicare coverage altogether and sign up for a Medicare Advantage plan, which is sold by a private insurance company (NOT the government)

Medicare Advantage is relatively new (it first became available in 2003), and while it started off a bit rocky, it’s more popular than ever today.

If you’ve seen any commercials or ads that mention $0 premium plans, Medicare HMOs or PPOs, dental and vision benefits with Medicare, or complimentary gym memberships, that’s all referring to Medicare Advantage.

By law, Medicare Advantage plans must cover what Original Medicare does, so you don’t have to worry about sacrificing coverage. In fact, most Medicare Advantage plans offer benefits above and beyond, including some dental and vision, gym memberships, and even funds you can use for over-the-counter items. Most Medicare Advantage plans also include drug coverage.

What's the downside of Medicare Advantage?

I’m sure you’re asking… what’s the catch?

There are a few things to be aware of:

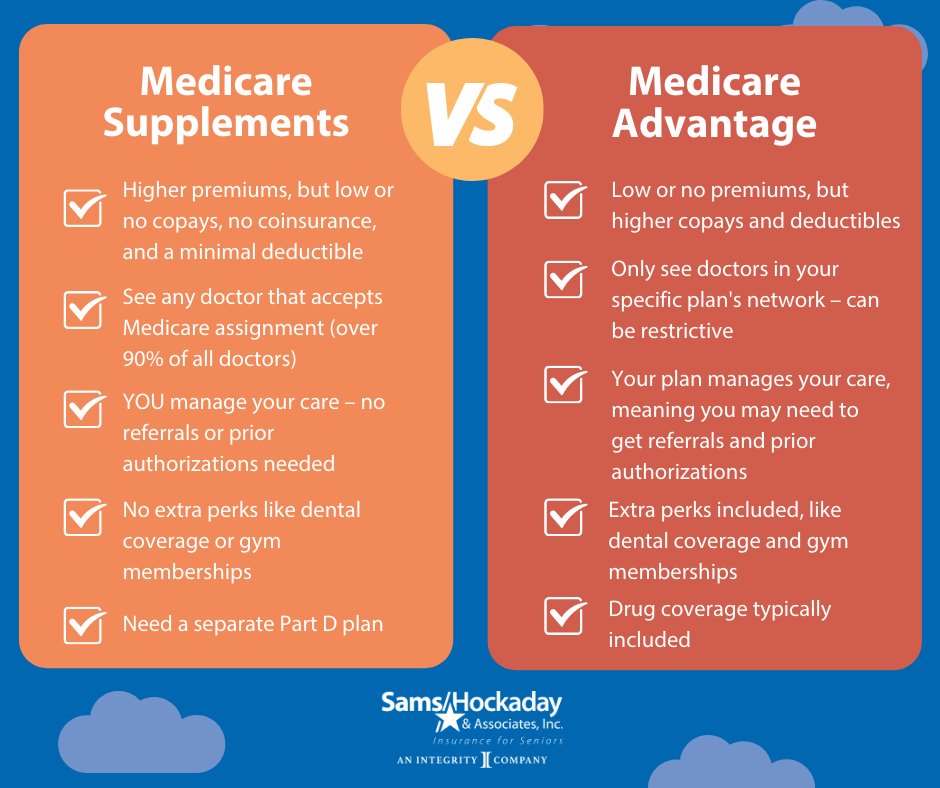

- You can think of Medicare Advantage plans as “pay as you go.” You have higher deductibles, copays, and coinsurance when you actually use the plan. With Original Medicare and a supplement, you pay a higher monthly premium, but have little to no out-of-pocket costs.

- Medicare Advantage plans have stricter provider networks than Original Medicare. Each plan is different, but the doctors and hospitals you can see will be limited. (Original Medicare is accepted by most (over 90%) of doctors.)

- Medicare Advantage plans are managed care, meaning the plan can dictate which doctors you see and what treatment you can get. The plan may ask you to try a cheaper treatment before approving a more expensive one. With Original Medicare, the coverage is fee-for-service, meaning you get whatever treatments you need – no prior authorizations required.

- The main health coverage may be exactly what you’re looking for, but the drug portion of the plan may not fit your needs. With Original Medicare, you can add a separate Part D plan, allowing you to tailor your coverage to fit exactly what you need, including your preferred pharmacy and the exact drugs you take.

As long as you fully understand the limitations of Medicare Advantage plans, they can be a benefit-rich alternative to Original Medicare.

In the Decatur, IL area, there simply haven’t been many options in the past. However, in the last two years or so, more insurance companies are coming to our area, which is allowing us to explore this option more seriously.

Read up more on MA plan options: 2021 Medicare Advantage Plans In Decatur, IL

How do I choose between Medicare Supplements and Medicare Advantage?

There's no cut and dry answer, because everyone's situation and preferences are different.

There are pros and cons to Medicare Supplements (Medigap) and Medicare Advantage. This chart helps clearly understand how they compare.

Most of our clients choose a Medicare Supplement (Plan G is the most popular plan), which has a lot to do with our location in central Illinois. Medicare Advantage plans are more competitive in big cities, whereas smaller cities and rural areas don't have as many options.

There's also more security in a Medicare Supplement. You have freedom to see almost any doctor, you can travel across the country without worrying about your insurance, and there are little to no out-of-pocket costs as you use the plan. It's predictable, and that's attractive to a lot of people we see.

However, Medicare Advantage plans are more popular than ever, and with $0 premiums and extra valuable benefits, they are worth considering!

You can schedule an appointment with an agent here at Sams/Hockaday to get specifics on what plans are available to you.

What does Medicare cover exactly?

The best way to find out what Medicare covers is to download the Medicare smartphone app, “What’s covered?”

If you have an Apple phone, here’s the link to download the app.

If you have an Android phone, here’s your link to download the app.

On this app, you can type in the name of a service or test, and it tells you if it’s covered or not.

We’ve also written many articles on our website about specific services – there always seem to be exceptions and convoluted information, so we interview doctors and get the real-life information you need to make informed healthcare decisions.

Check out:

- Podiatry: Does Medicare Cover Foot and Ankle Treatment?

- Does Medicare Cover Hospice?

- Does Medicare Cover the Shingles Vaccine in Decatur, IL?

- Does Medicare Cover Out of Country Healthcare?

- Acupuncture: What Is It and Does Medicare Cover It?

- Does Medicare Cover Medical Marijuana?

- Glasses, Contacts, and Eye Exams: Does Medicare Cover It?

- Orthopedics: What Is It, and Does Medicare Cover It?

- Does Medicare work with concierge medicine services?

- Does Medicare Pay for Hearing Aids, Hearing Exams, or Balance Exams?

How do you sign up for Medicare?

Social Security enrolls you in Original Medicare (Parts A and B).

Signing up for Medicare is simpler than ever – you can do it online via the Social Security website. Visit the Medicare page and scroll down to the blue “Apply for Medicare Only” button.

For most people, you’re eligible for Medicare starting three months before your 65th birthday. That “initial enrollment period” lasts until three months after your 65th birthday.

DON’T MISS THAT ENROLLMENT WINDOW! If you do, you may pay a higher Medicare premium for the rest of your life, and the markup isn’t cheap.

Conclusion

We encourage everyone who is getting close to Medicare to contact us.

Missing deadlines is a common mistake people make, and it can cost you in the long run. Plus, we can help answer all of those specific, personalized questions, like:

- What if I’m still working and don’t need Medicare yet?

- What if I'm a veteran?

- What if I get health insurance in retirement through the state?

- What if I’m a retired teacher?

- What if I have money in an HSA?

- What if I worked for the railroad and get their benefits now?

We can help with all of those personal situations. That’s what we’re here for!

Plus, our service is free. You can learn more about how we get paid here: How Agents Get Paid

To schedule an appointment with a licensed agent, visit our online scheduling page! You can also start a website chat during normal business hours or fill out our contact form to connect with us.

Schedule an Appointment

Book time right on our agents' calendars using our online scheduling system.

Choose Appointment

Here's what our clients say…

Meet Our Agents