How Income Affects Your Medicare Costs In 2026

Many new-to-Medicare individuals are shocked when they find out Medicare isn’t free after all. Plus, the more money you make, the more you pay for Medicare.

If you have a high income, here’s a look at what Medicare will cost you in 2026 and how you can plan accordingly.

Calculate Your Medicare Costs Today

Create a Medicare action plan by estimating your total monthly premiums for healthcare and related expenses in retirement.

Get My Worksheet

Many people are surprised to learn that Medicare isn’t completely free.

And on top of that, while most beneficiaries pay the standard premiums, your income can play a role in how much you pay. If your income is above certain limits, Medicare premiums can increase.

Here’s what higher-income beneficiaries can expect to pay in 2026, and the steps you can take to plan ahead.

Do Certain People Really Pay More for Medicare?

Yes — some people do.

In 2026, the standard monthly premium for Medicare Part B (medical insurance) is $202.90. Many people also pay a separate premium for a Medicare Part D prescription drug plan.

Most Medicare beneficiaries pay the standard Part B amount. However, CMS estimates that about 8% of people with Medicare pay a higher premium because of their income.

This extra charge is called an Income-Related Monthly Adjustment Amount (IRMAA). It’s not a separate plan or penalty — it’s simply an additional amount added to your Medicare Part B and Part D premiums if your income is above certain limits.

Medicare determines whether IRMAA applies by looking back two years at your tax return. That means whether you’ll owe an IRMAA in 2026 depends on the income you reported for 2024.

If you fall into this higher-income group, Social Security will mail you an Initial IRMAA Determination notice explaining whether you’ll pay higher Medicare premiums and how much more you’ll owe.

If an IRMAA applies, the extra amount is usually deducted from your Social Security benefits. If you’re not receiving Social Security yet, Medicare will send you a bill.

At What Income Level Do Medicare Premiums Increase?

Since Medicare looks back two years, your 2024 income is used to determine whether you’ll pay higher Medicare premiums in 2026.

- If you file taxes individually and your 2024 income was higher than $109,000, your 2026 Medicare premiums will increase.

- If you’re married and you file taxes jointly and your 2024 income was higher than $218,000, you’ll also pay more for Medicare.

Also, Medicare looks at your modified adjusted gross income (MAGI) – that number isn’t actually on your tax return.

To calculate MAGI, Medicare starts with your adjusted gross income (AGI) from Form 1040, then adds back certain deductions, including:

- IRA deductions

- Deductions you took for student loan interest or tuition

- Passive income or loss

- Excluded foreign income

- Rental losses if you’re a landlord

- Interest from EE savings bonds used to pay college expenses

- Half of your self-employment tax

- Employer-paid adoption expenses

- Any losses from a publicly traded partnership

For many people, their MAGI will be higher than their adjusted gross income. However, if you don’t have any deductions to add back, it could be the same number.

If we lost you at MAGI and you’re concerned about income-related premium increases, your tax advisor can help you determine the number Medicare uses.

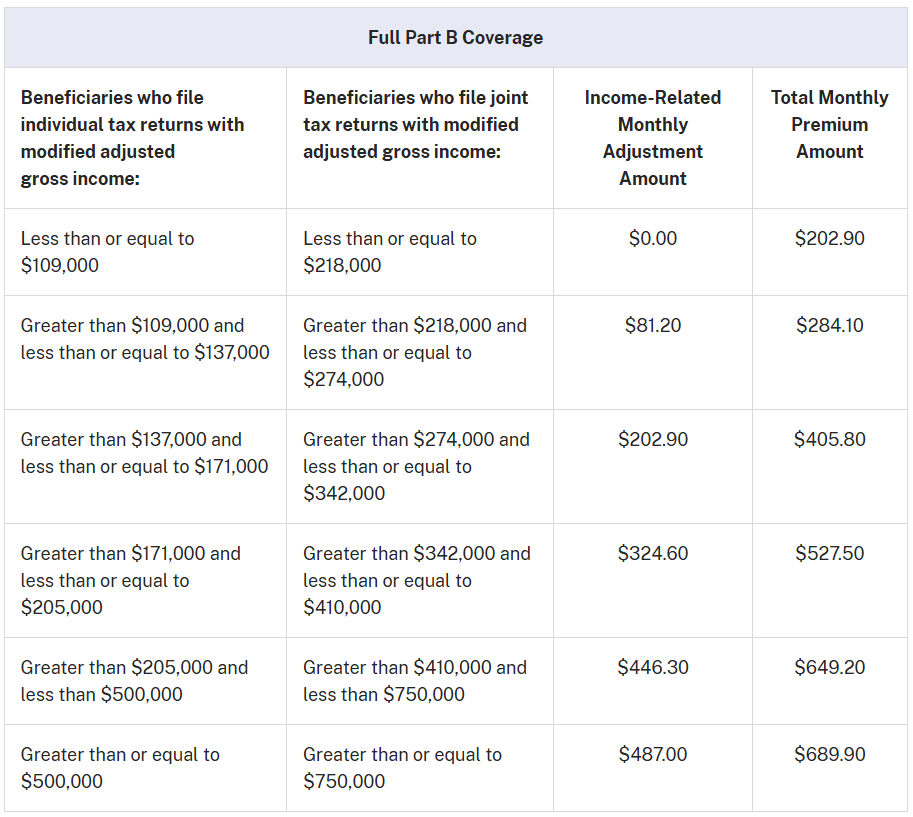

What Are the Medicare Premiums Based on Income for 2026?

There are five higher-income Medicare brackets. If you fall into one of these brackets, you’ll pay an Income-Related Monthly Adjustment Amount (IRMAA) for Medicare Part B and, if you have a Part D plan, an additional surcharge for Medicare Part D.

2026 Part B premium surcharges for high incomes

Depending on how high your income is, you could pay between 40-240% more for Medicare Part B.

The standard Part B premium in 2026 is $202.90 per month. Based on your income bracket, your monthly Part B premium could range from $284.10 up to $689.90.

Higher-income beneficiaries who have only immunosuppressive drug coverage, or who are married filing separately may have different adjusted amounts.

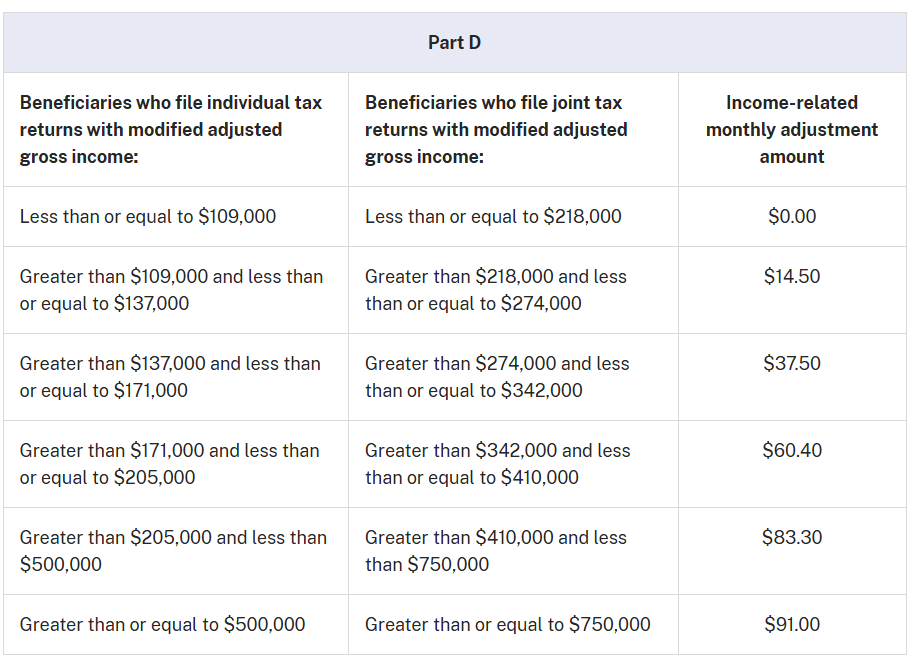

2026 Part D premium surcharges for high incomes

Medicare Part D premiums vary depending on which plan is best for you and your prescriptions.

If you want to compare Medicare Part D plans, our step-by-step guide make it easy to evaluate Part D plan costs, covered medications, and preferred pharmacies so you can see which option best fits your needs.

Regardless of your plan’s premium, if you fall into one of Medicare’s five higher-income brackets, you’ll have an extra premium on top of your regular one.

The first income bracket will have an extra $14.50 added to their plan’s premium, and the highest bracket will have to pay an additional $91.00:

So, if your drug plan were $20 per month, you could potentially pay up to $111 for your Part D plan because you have a high income.

Those who are married filing separately would have different adjusted amounts.

How Do I Reduce My IRMAA?

If you know your MAGI will qualify you for higher Medicare premiums, there are a few steps you can take to potentially reduce your IRMAA, or the surcharge you pay for having a high income.

Reduce your MAGI

Because the adjustments are based on your income, the best way to avoid IRMAA is to reduce your annual income. Keep in mind the IRMAA is based on your tax return from two years ago, so working with a financial planner well in advance is the best way to ensure your Medicare premiums won’t cripple your retirement plan.

If you’re worried about your IRMAA (income-related adjustments that increase your Medicare premiums), don’t make significant financial changes that will increase your taxable income.

For example, avoid:

- Selling real estate

- Selling large amounts of stock

- Taking large distributions from retirement accounts

- Converting traditional IRAs to Roth IRAs in one big transaction

A financial advisor can also keep a close eye on vested and restricted stocks to ensure your income doesn’t increase too much in that two-year lookback period.

Report a life-changing event

If you’ve had a life-changing event that has reduced your income in the last two years, you can let Medicare know. They might reduce your IRMAA if you’ve:

- Gotten married

- Gotten divorced

- Lost your spouse

- Lost your job

- Lost an income-generating property

- Lost your pension

- Got a settlement from an employer

If any of these events have happened to you in the last two years, you can request to lower an Income-Related Monthly Adjustment Amount by completing the IRMAA Life-changing event form and taking it to your local Social Security office.

Make a donation

Under certain circumstances, you can donate your required minimum distributions (RMDs) to avoid having them counted as part of your income. If you don’t need that income, donate it to a qualified charitable organization.

If you go this route, ensure the check is written directly to the charity to ensure it’s not counted as part of your income.

Conclusion

Higher-income earners pay more for Medicare Parts B and D.

If you're concerned about IRMAA or unsure if it will affect you, give us a call—we’ll help you understand your Medicare costs and explore your options.

You can also use our Medicare Cost Worksheet to estimate your expenses. Simply plug in your numbers and refer to the handy IRMAA chart for a clear breakdown of your cost estimates.

Calculate Your Medicare Costs Today

Create a Medicare action plan by estimating your total monthly premiums for healthcare and related expenses in retirement.

Get My WorksheetHere's what our clients say…

Meet Our Agents